.avif)

Bitcoin Staking vs. BTC Lending: Why Custody Is the First Question

There are three ways to earn yield on bitcoin today. In one, you give your BTC to a company. In another, you send it across a bridge to another chain. In the third, it stays on Bitcoin, under your keys, the entire time.

The differences between these approaches are not cosmetic. They determine what happens to your bitcoin if something goes wrong. When evaluating any product that offers yield on BTC, the first and most important question is not about the APY. It is about custody: who holds the bitcoin, and under what conditions.

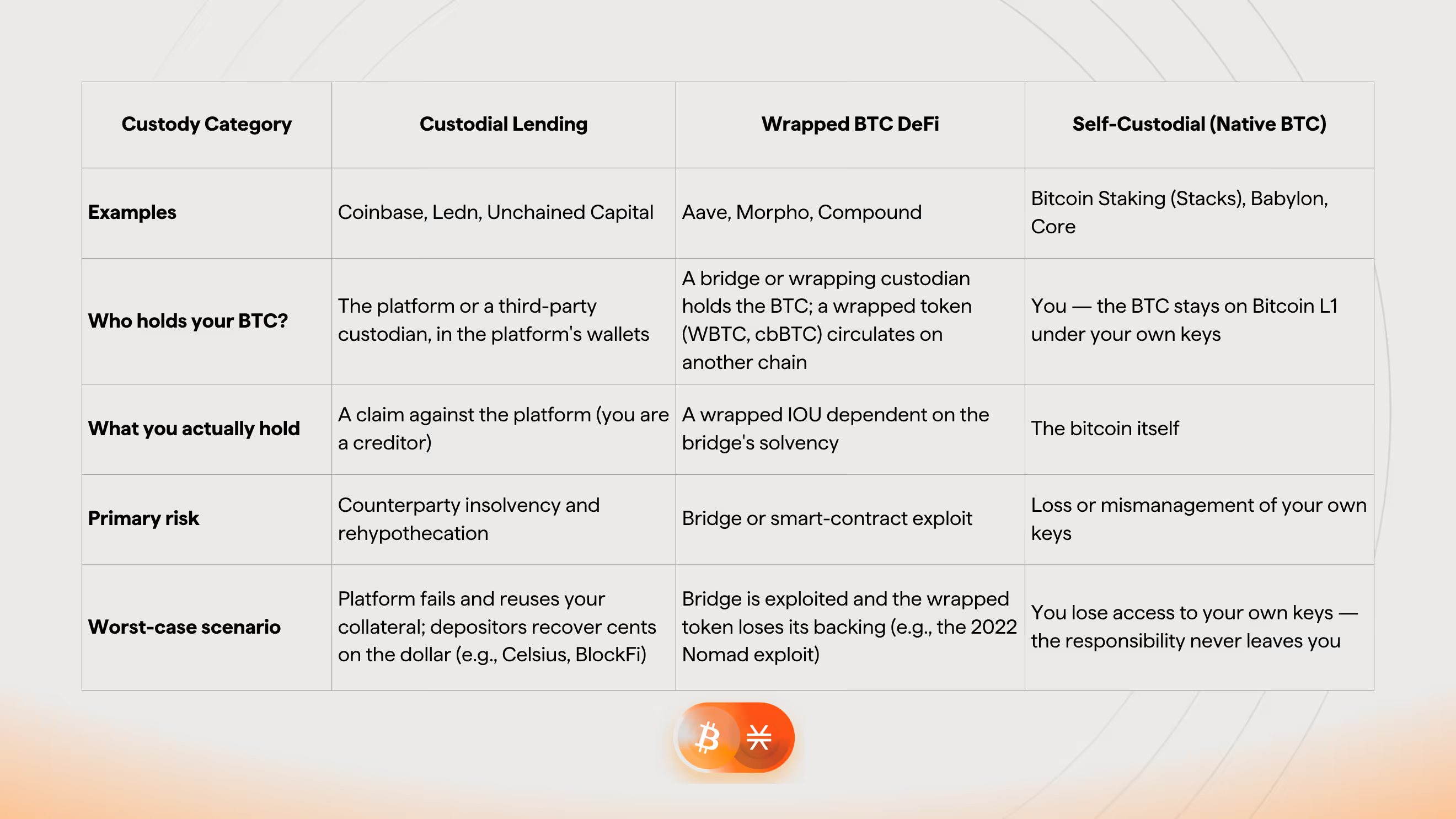

The Custody Spectrum

Every BTC yield product falls somewhere on this spectrum:

Custodial Lending: The Structural Problem

Custodial lending platforms operate a straightforward model: users deposit BTC, the platform lends it out or invests it, and users receive yield from the spread. The issue is not the yield mechanism itself but the custody transfer. Once bitcoin is sent to the platform's wallet, the depositor holds a claim rather than an asset. If market conditions deteriorate and the platform cannot meet its obligations, depositors are creditors, not holders.

This is not a hypothetical risk. It is a structural feature of any model that requires transferring bitcoin to a third party before yield can be earned.

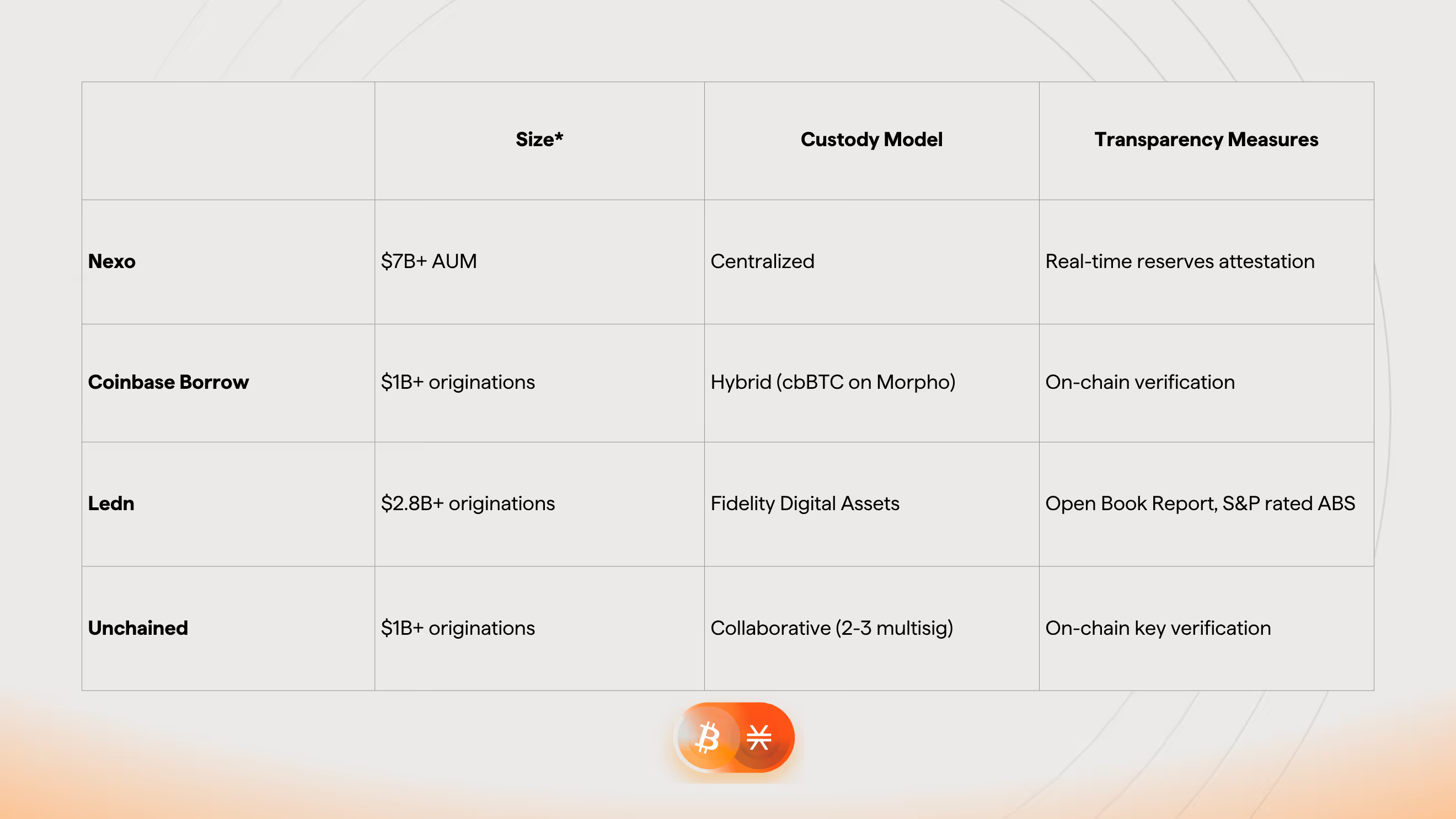

The custodial lending market has rebuilt itself since the last cycle, with outstanding crypto-collateralized loans reaching roughly $73.6 billion by Q3 2025. Leading players include Nexo (over $7 billion in AUM) and Ledn ($2.8 billion-plus in originations since 2018). After the 2022–2023 collapses, many firms now prohibit rehypothecation, use qualified custodians, and publish proof-of-reserves attestations. But even within custodial lending, custody models vary.

*as of May 2026

Wrapped BTC in DeFi: Improved, but Incomplete

Products like wBTC in Ethereum DeFi moved the custody question but did not resolve it. BTC is locked with a custodian, bridge, or smart contract and the depositor receives a wrapped token on another chain. Yield can be earned in DeFi with that token, but the underlying bitcoin remains with the bridge operator.

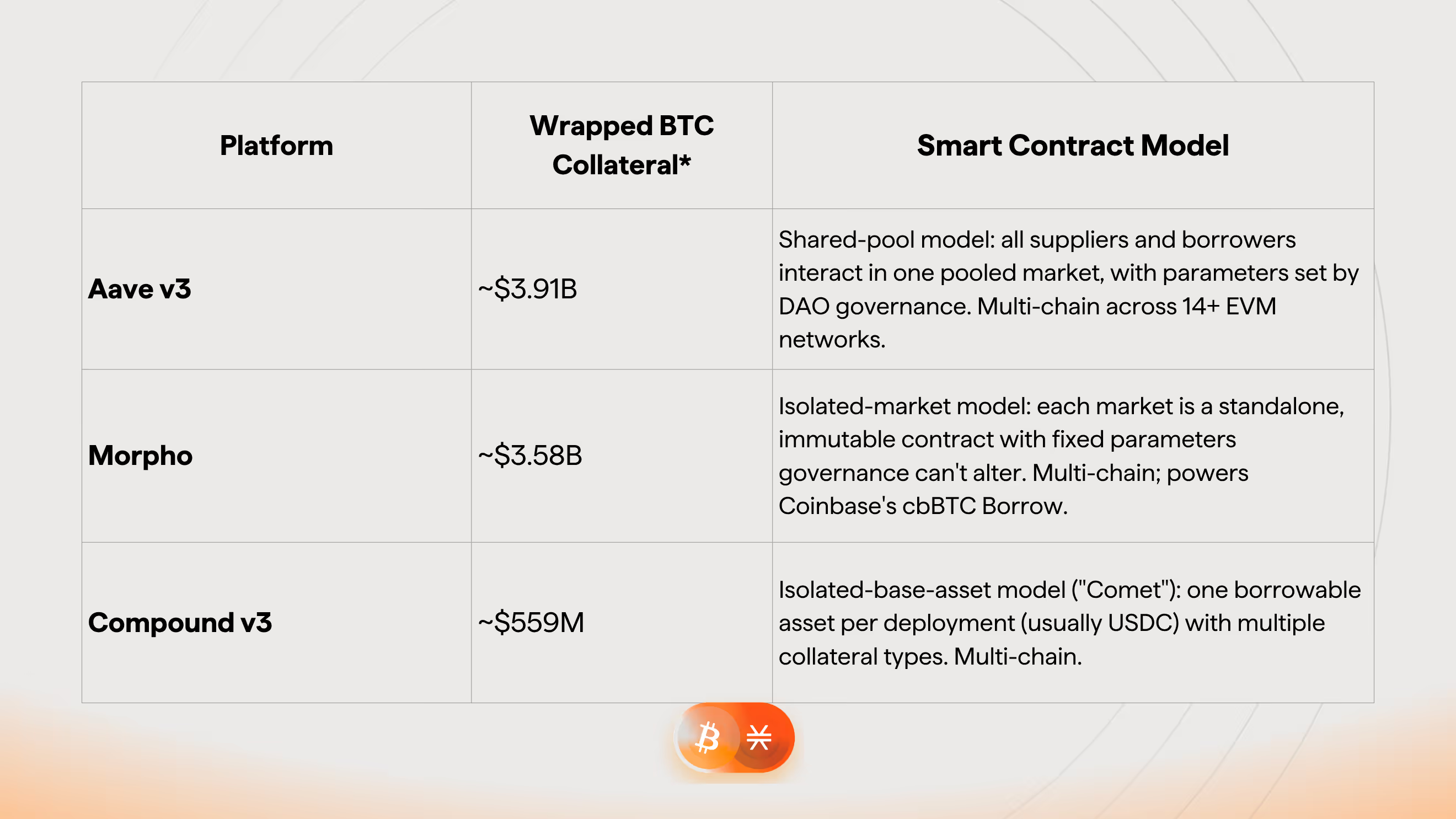

The wrapped-BTC DeFi lending market is concentrated among a few protocols: Aave ($40B+ TVL), Morpho ($10B+), and Compound (~$2B), all accepting WBTC and cbBTC as collateral. Morpho built on Aave and Compound before evolving into its own modular primitive, and now powers Coinbase's cbBTC-backed "Borrow" product.

The model's weakness is the wrapper itself — bridges remain crypto's most exploited infrastructure, with the 2022 Nomad exploit alone draining ~$24 million in WBTC. The fundamental issue persists: the bitcoin is not on Bitcoin.

*as of May 2026

Bitcoin Staking: Custody Does Not Transfer

Bitcoin Staking is the third way to earn yield on your bitcoin. It is not a lending product since no one borrows your BTC, and you are not a creditor waiting to be repaid. It is something different: your bitcoin stays on Bitcoin L1, under your own keys, and earns yield from network activity rather than from someone else taking the other side of a loan.

Bitcoin Staking on Stacks takes a structurally different approach:

- BTC is locked on Bitcoin L1 using a standard timelock (OP_CHECKLOCKTIMEVERIFY), a script in production since 2015. The holder's keys, the holder's wallet.

- The timelock is enforced by Bitcoin consensus, the same rules that govern every other Bitcoin transaction.

- No party can move the BTC during the bonding period. Not Stacks, not a bridge operator, not a smart contract on another chain.

- At maturity (approximately six months), the timelock expires and the BTC is available again.

There is no custody transfer at any point in the process. The yield comes from Stacks miners bidding BTC through Proof of Transfer, a mechanism that has operated continuously since January 2021. Yield is generated by miner activity, not by lending the depositor's bitcoin.

Stacks is not the only protocol bringing self-custodial yield to native Bitcoin. Babylon — the largest by far, with over $5.6 billion in BTC staked — and Core both let holders stake native BTC to secure proof-of-stake networks without bridging or wrapping. But the yield is paid in the secured network's own token, not bitcoin, and neither offers a lending product. They are staking protocols, not credit markets.

That gap is where Stacks is different: the same architecture that keeps staked BTC on L1 is also the foundation for self-custodial bitcoin lending. Zest, a lending hub in the Stacks ecosystem, already offers Bitcoin-backed borrowing with 800+ BTC and 41,000+ users, while Granite provides Bitcoin-backed borrowing with no rehypothecation, isolated collateral per position, and soft liquidations designed to preserve your BTC. Neither is fully self-custodial yet — both rely on sBTC rather than native L1 BTC — but they prove the lending demand and infrastructure already exist. Once Bitcoin Staking launches, the same custody model that lets BTC earn yield on L1 can extend to borrowing against it, without ever transferring the coins.

The Tradeoffs

Bitcoin Staking involves tradeoffs relative to other yield approaches, and these should be understood clearly.

- Lower yield: The target is approximately 3% APY. Some lending platforms and DeFi strategies offer higher nominal rates. The yield from Bitcoin Staking is more modest because it derives from a sustainable, verifiable source rather than from leverage or duration mismatch.

- STX requirement: Creating a protocol bond requires locking STX worth 5% of the BTC position. This is an additional asset to acquire and hold. Lending platforms and wrapped BTC DeFi do not have this requirement.

- Illiquidity: BTC is locked for approximately six months. Lending platforms typically offer more flexibility. The sBTC path on Stacks provides some DeFi composability, but native L1 positions are locked for the full term. There is an "Early Exit" option where the BTC is released but the STX position stays locked for the full term of the protocol bond.

What these tradeoffs provide in return is that the bitcoin remains on Bitcoin, under the holder's own keys, for the entire duration. For many BTC holders, that is the determining factor.

The Question to Ask

When evaluating any BTC yield opportunity, the first question should be: where is the bitcoin right now, and who controls it? If the answer is anything other than "on Bitcoin, under the holder's own keys," the strategy involves a custody transfer, and the associated risks should be evaluated accordingly.

Read the full Bitcoin Staking Whitepaper.

Read next: The Risk Profile of Bitcoin Staking Explained | How to Earn Yield Without Giving Up Custody

Get more of Stacks

Get important updates about Stacks technology, projects, events, and more to your inbox.