.avif)

7 Institutional-Grade Features of Bitcoin Staking on Stacks

The Bitcoin Staking whitepaper introduced a new model for earning yield on bitcoin. Here are seven features that define how it works and why it's built differently.

1. Yield is paid in BTC

Most Bitcoin staking protocols pay yield in their own token. CoreDAO pays in CORE. Babylon pays in BABY. The effective return depends entirely on the reward token holding its value, a risk that has nothing to do with Bitcoin and everything to do with a separate token's market dynamics.

Bitcoin Staking on Stacks pays yield in BTC. The return is denominated in the same asset that was staked. There is no secondary token price risk on the yield itself. When the yield and the principal are the same asset, the math is simple and the risk model is clean.

2. BTC never leaves Bitcoin

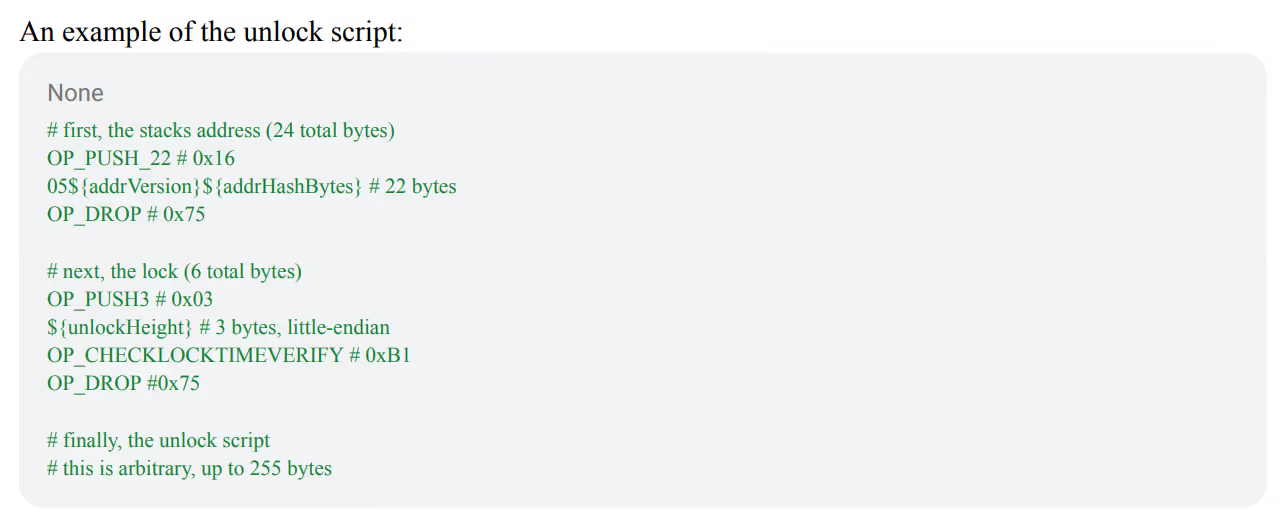

The participant's bitcoin stays on Bitcoin L1 for the entire bonding period, locked using OP_CHECKLOCKTIMEVERIFY, a standard Bitcoin script in production since 2015. The keys remain with the participant. The protocol cannot move the bitcoin. There is no bridge, no wrapper, and no smart contract on another chain holding the asset.

This is not "self-custodial" with an asterisk. The bitcoin is on Bitcoin. The keys to your bitcoin are yours for the full term.

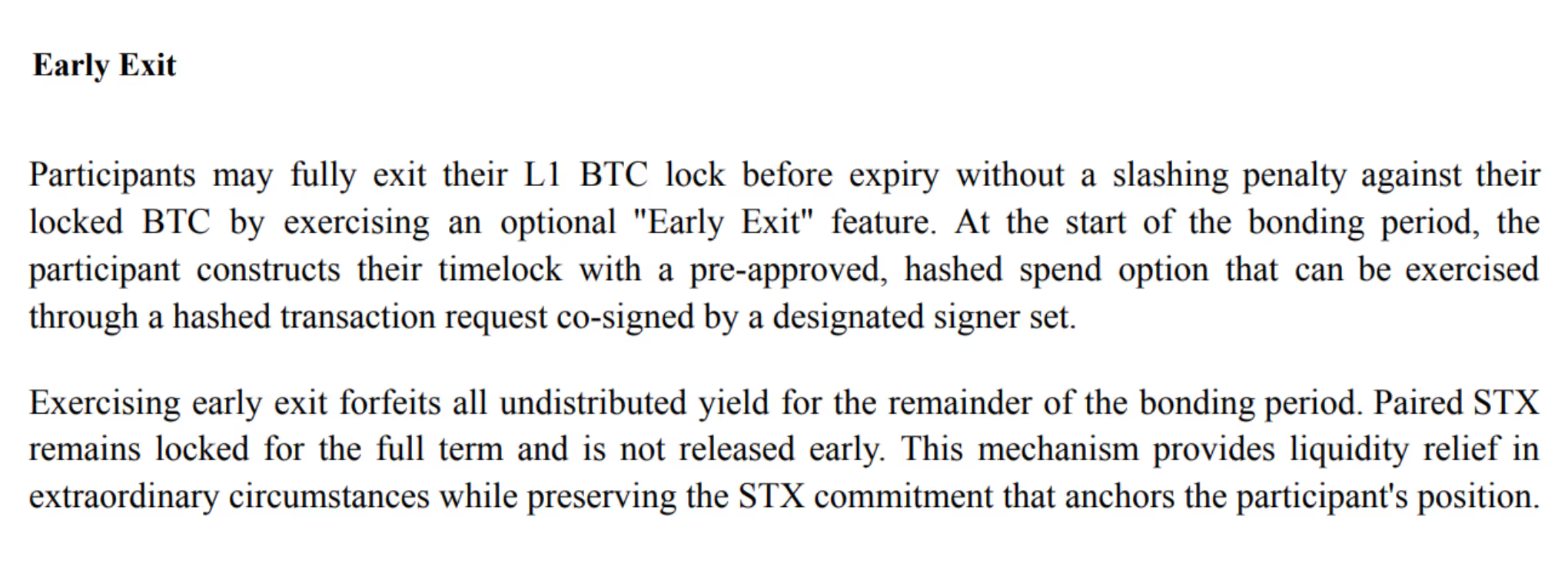

3. Early exit is available

This is the feature the market is underestimating.

BTC is timelocked for the bonding period (approximately six months), but the whitepaper includes an early exit mechanism. A participant can request to have their BTC unlocked and returned at the next Bitcoin block, roughly 10 minutes.

The tradeoff is straightforward: remaining yield is forfeited, and the paired STX stays locked for the full term. But the bitcoin comes back. The BTC lock is a technical mechanism, not a binding obligation like collateral on a loan. The only position without an exit option is the STX side.

For any treasury or fund manager evaluating this, the distinction matters. Participants have a defined path to recover principal if conditions change. That changes the liquidity profile of the entire product.

4. No slashing

In delegated proof of stake systems, staked assets can be partially or fully destroyed if a validator misbehaves. Principal is at risk based on someone else's behavior, and the participant has no control over the outcome.

Bitcoin Staking has no slashing mechanism. Principal is returned in full at the end of the bonding period. Yield may vary with market conditions, but principal does not. For participants coming from traditional fixed income, this is closer to a bond than a stake.

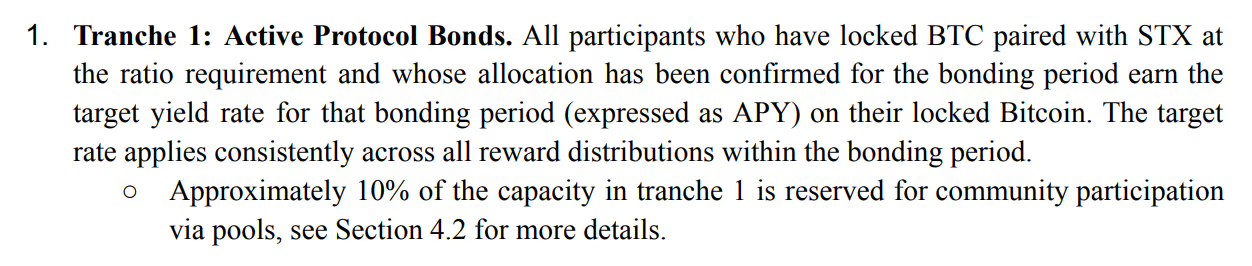

5. Yield distributed via waterfall structure

Bitcoin Staking uses a waterfall structure similar to institutional structured credit products. Protocol bond holders are paid first from each reward cycle's miner BTC pool, at a uniform clearing rate set by auction. The protocol bond holders have first claim on the yield pool every cycle.

STX-only stakers are paid next and a reserve fund is maintained to buffer cycles where miner revenue falls short.

The target APY is approximately 3%, algorithmically adjusted based on miner economics and coverage ratios. It is a target rather than a contractual guarantee, but the structure is purposefully built to deliver consistency. The language is borrowed from institutional finance because the mechanics are too.

6. The yield source has 5+ years of production history

The mechanism behind Bitcoin Staking is not new. Stacks' Proof of Transfer consensus has been live since January 2021. Miners have been committing BTC approximately every 10 minutes to compete for block rewards for over five years, distributing more than 4,200 BTC to participants.

Bitcoin Staking structures this existing yield source rather than creating a new one. All activity is recorded onchain on Bitcoin and independently verifiable. In an industry where most yield products are months old, five years of continuous production data is a meaningful differentiator.

7. Risk management is built into the protocol

The system does not rely on market conditions staying favorable. It actively monitors and adjusts:

Coverage ratio monitoring

The protocol tracks the ratio of available miner revenue to bond obligations across five response bands (from "excess" above 2.0x to "critical" below 0.8x). Each threshold triggers automatic adjustments without governance votes.

Reserve fund

15% of excess miner revenue is set aside to buffer future cycles where miner bids decline. The reserve is drawn before any bond holder misses a payment.

Capacity constraints

Each bonding period has algorithmically determined capacity. The protocol does not issue more bonds than the yield pool can support.

Staged launch

The bootstrap phase (PoX-5) launches with vetted partners before expanding to fully permissionless operation (PoX-6), allowing the system to build a track record under controlled conditions.

These mechanisms are core to the protocol design and map to the risk frameworks institutional participants expect. The protocol is designed to perform in downturns, not just in favorable conditions.

Summary

These seven features, taken together, represent a combination that does not currently exist in any other BTC yield product: yield paid in BTC, full self custody on Bitcoin L1, an early exit mechanism, no slashing, structured yield priority, a proven yield source, and built in risk management.

The full specification is in the whitepaper.

Explore the Bitcoin Staking Resource Hub.

Get more of Stacks

Get important updates about Stacks technology, projects, events, and more to your inbox.